Goods and service tax though is a big indirect tax reform in India post-independence but in reality, it is a business process reform. One of the major drawbacks with the current taxation is, it is not a multi-point tax as in Central Excise where the input tax credit can be taken only by the registered dealer who is having an element of manufacturing. This results in more price to be paid by the end consumer as the ITC is not available in the whole distribution cycle. In Goods and Service Tax, the ITC is available and this results in lower taxes and resulting in the customer at a lower price.

With the rollout of GST, the prices are supposed to come down on the availability of ITC at all stages, if the same is not passed on to the end customer, there is a stringent monitoring mechanism to ensure that the same is passed through the Anti profiteering clause. Though the details of same are not announced the industry has to be prepared to brace the same and in this, the role of cost and management accounts is very critical. No other professional can prepare a cost sheet in a perfect manner other than cost accountant. With the GST rollout from 1st July 2017. The cost auditor or the cost accountant can prepare a cost sheet for prior to the rollout of GST with the existing taxes and also clearly mark the elements of tax which is not available for credit under existing system along with the expected cost in GST. As the rates are also available in the public domain, the tentative cost sheet for the item can be prepared. This will give a fair idea to the organization on the pricing policy to be taken post GST with the effective ITC available. If the same activity is not done prior to the rollout of GST, there is huge possibility that the competitor must have done this activity and result in a lower price from his side, if the competitor price is lesser than then our price, then it will directly impact the top line and the bottom line of the organization.

Section 171 of the Central Goods and Service Tax describes the Anti-Profiteering clause

- (1) Any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.

(2) The Central Government may, on recommendations of the Council, by notification, constitute an Authority, or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

(3) The Authority referred to in sub-section (2) shall exercise such powers and discharge such functions as may be prescribed.

For the vested interest of the organization, the same should be considered and tentative pricing should be ready based on the current scenario and once it done and after the rollout the same can be visited with the ground reality and the cost sheet is to be reworked, this process will ensure that same top line is maintained even after rollout of GST or improved also.

The cost accountant while preparing the cost sheet should keep in mind that the input tax credit can be taken only on supplier’s payment of taxes and matching of the tax returns of the supplier and recipient, this will involve some cost and the same should be factored. The costs to be factored are the additional working capital requirements, compliance cost for return filing as the GSP/ ASP has to be paid for the return filing services and also for the additional cost involved for reconciliation. This cost will be in form of additional manpower or additional software requirements or by way of outsourcing the same.

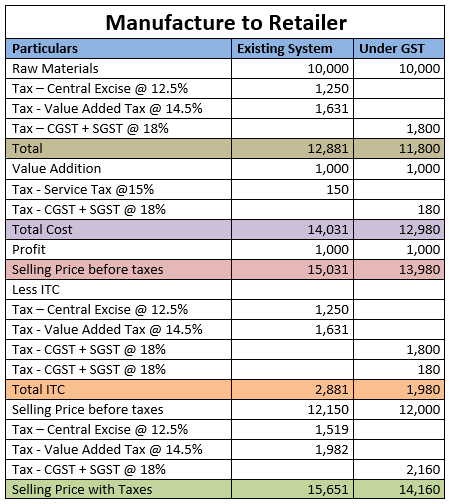

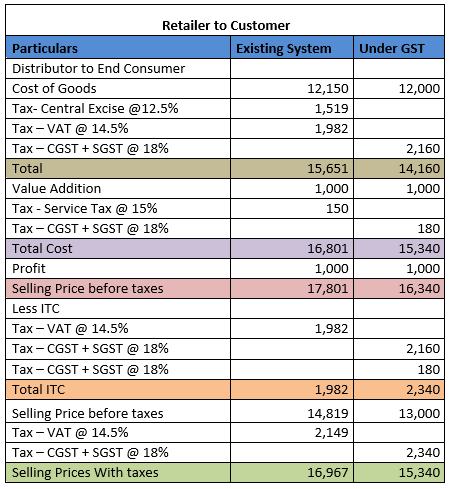

Given below is the table which gives a comparison of cost pre and post rollout of GST without additional compliance cost being factored in.

It is clearly visible that the post-rollout of GST, the prices are going to come down only on the account of tax treatment, so the government is also keen to pass on the same to the common man for this the Anti-Profiteering clause is introduced in the GST Acts. The clue for this is taken from the Malaysian GST where the industry has not passed on the tax benefits to the customers and this has resulted in a lot of unrest in the society as well as higher inflation. To avoid all these drawbacks, we have the anti-profiteering clause and at this point in time, we do not have any guidelines on what basis the government will serve notice and what documentary evidence we need to provide in such cases.

Keeping in view of that it is recommended to have the cost sheets ready so that the trade and industry need not run for information at that point in time. This is should be one of the activities for the transition/planning for GST.

The recommendations for the cost and management account will be very useful to the trade and industry and indirectly the role of cost and management accounts even though in industries where cost audit is not mandatory. The anti-profiteering clause has made it mandatory for all industries to maintain cost sheets without any cost audit indirectly.

In the second table as we have discussed we need to add the costs for the working capital and compliance costs on account of GST, this will give a clear indication on the profit. The same can be revised when the actual number are available after the rollout of GST on monthly basis or quarterly basis or on the organizational requirement at regular intervals.

Similar cost sheet has to be prepared for services also be it in the banking sector or telecom sector..this activity will help in determining the exact cost impact and the basis on which it can be passed on to customers.

Any views or opinions represented above are personal and belong solely to the author and do not represent those of people, institutions or organizations that the author may or may not be associated with in professional or personal capacity unless explicitly stated. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

Good analysis and explained very well Thanks for the article l…..this clause will give certainly good opportunity to Cost & Management Accountants.

LikeLiked by 1 person

Yes we much true, it only depends on how we do utilize the opportunity given to us

LikeLike

Excellent presentation with simple analysis.

LikeLiked by 1 person

Thanks a lot for your feedback

LikeLike

Hi , Maybe I am wrong but In your example, You show both Taxes (Service and VAT) for current scenario, I don’t think that is right if it is two different thing than the tax is 36% (18 %) on both.

Have you taken the real sample?

LikeLiked by 1 person

Kamal, you are correct normally when there is VAT you do not have service tax. In the example, i have added the value addition which i am considering them as marketing costs, advertising costs, rent etc on which you service tax. For ease of understanding i have taken this even the numbers also

LikeLike